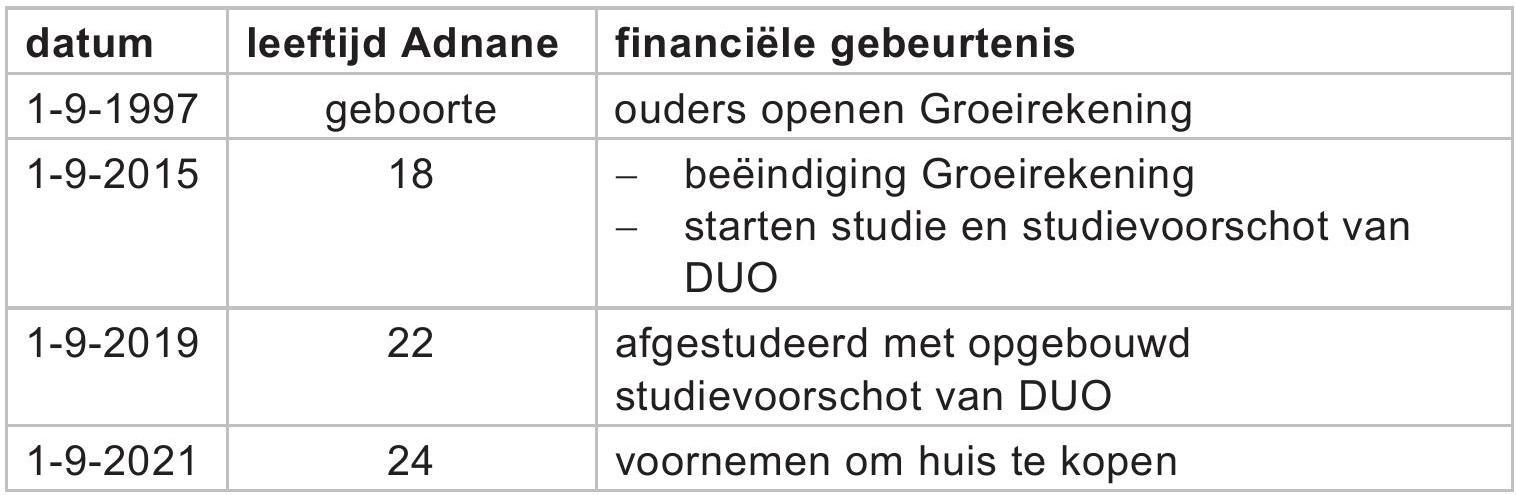

Bij deze opgave horen de informatiebronnen 4 tot en met 6.

Adnane heeft te maken met de volgende financiële gebeurtenissen:

Bij deze opgave horen de informatiebronnen 4 tot en met 6.

Adnane heeft te maken met de volgende financiële gebeurtenissen:

Op deze pagina behandelen we vraag 25 van het centraal examen bedrijfseconomie havo 2022 – tijdvak 3. Deze vraag is onderdeel van Opgave 5, en is 3 punten waard.

Je kunt hier zelf het antwoord invullen en vervolgens direct de uitwerking en uitleg bekijken.

Daarnaast kun je:

De onderwerpen bij deze vraag zijn: